Market Overvalued? Let's Look Under the Hood

Three reasons why traditional valuation metrics are misleading, and what could make them irrelevant.

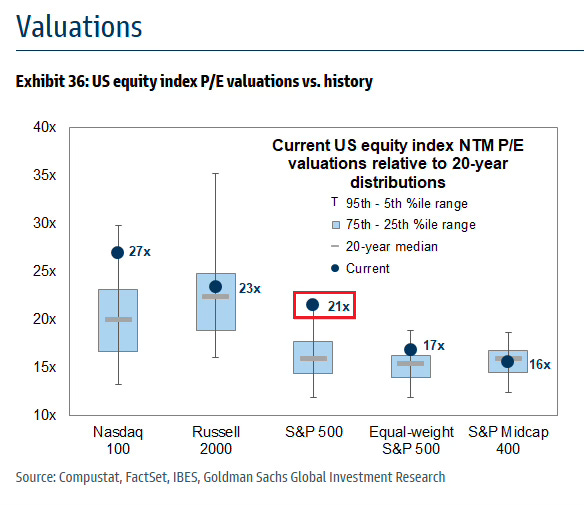

Everywhere I look lately, especially in the more traditional corners of financial commentary, I see the same old charts and hear the same old warnings: "Stocks are historically overvalued!" They’ll point to the Price-to-Earnings (P/E) ratio of the S&P 500, show how it’s well above its long-term average, and imply that a crash is just around the corner. You can't argue with the charts showing a high P/E, but I don't think the conclusion is that simple. In fact, I think looking at the S&P 500's overall P/E ratio in isolation tells you very little about what's really going on or where we might be heading.

To me, there are some pretty clear structural reasons why today’s seemingly high valuations might be justified. And beyond that, there’s a technological tidal wave building that could make even these valuations look cheap in hindsight. And yes, I know that’s what everyone said before the dot-com bubble. But hear me out.

Part 1: Why Today's "High" Valuations Might Be Perfectly Rational

Before we get to the future, let's talk about why the current market structure makes a higher average P/E more normal than many think. There are three main themes at play:

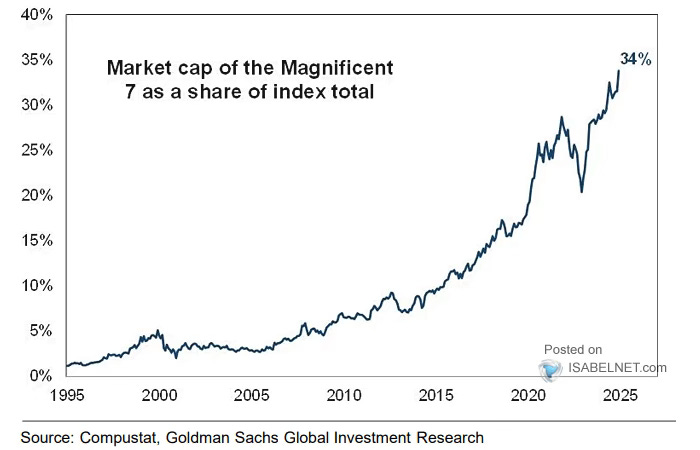

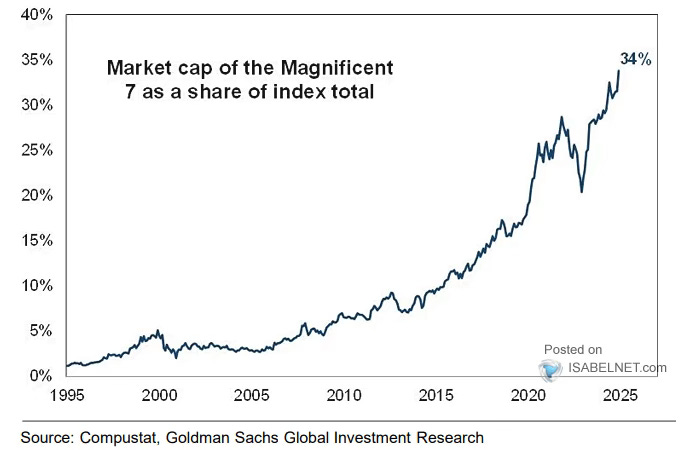

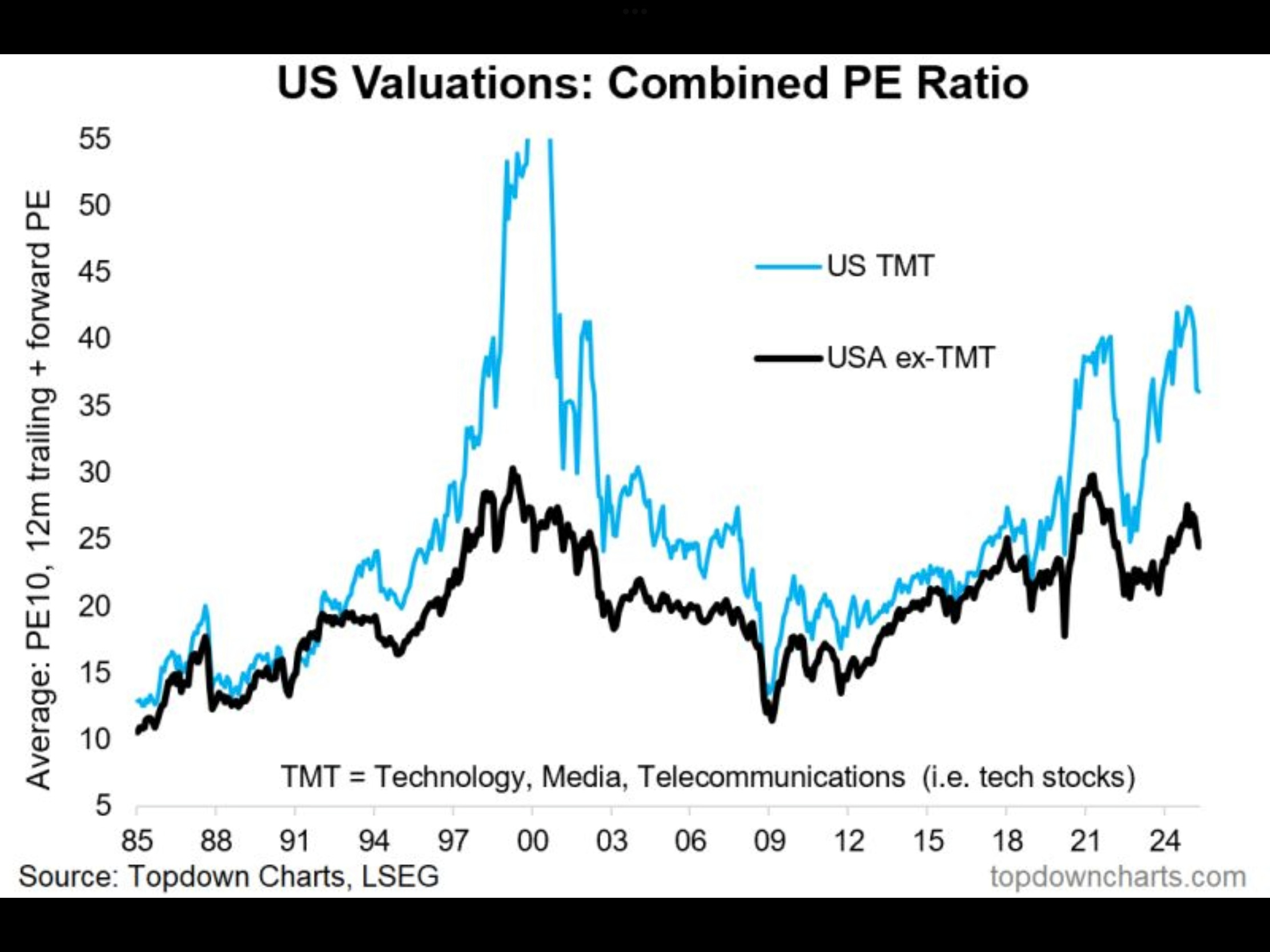

The Great Concentration: Big Tech is Eating the World (and the Index): It's no secret that growth, particularly earnings growth, is becoming increasingly concentrated in a handful of dominant technology companies – the so-called "Magnificent 7" and their peers. These companies are genuinely expanding their share of the overall economic pie due to network effects, superior technology, and massive scale. Their earnings are growing at a rate that genuinely justifies high P/E ratios - much higher than the typical S&P 500 average. These aren't your granddad's industrial conglomerates; these are global platforms with unprecedented reach and profitability.

When Giants Tilt the Scales: Index and Valuation Weighting: Following on from the first point, as Big Tech companies become a larger percentage of the S&P 500 (currently, the Mag 7 alone make up about 34% of the index's market cap), their valuations naturally have a much larger influence on the overall index's P/E ratio.

Historically, fast-growing, highly profitable technology companies with strong competitive advantages have always commanded higher P/E ratios than, say, stable utility companies or industrial firms. So, if the index is increasingly made up of these higher-growth, higher-P/E-multiple tech stocks, the average P/E of the entire index is bound to be higher than it was when the index was dominated by different kinds of businesses. It's simple math. Comparing today's S&P 500 P/E to the average from 30 years ago is an apples-to-oranges comparison.

It’s also worth mentioning Tesla’s P?E of 190 will alone be adding significantly to the average too.

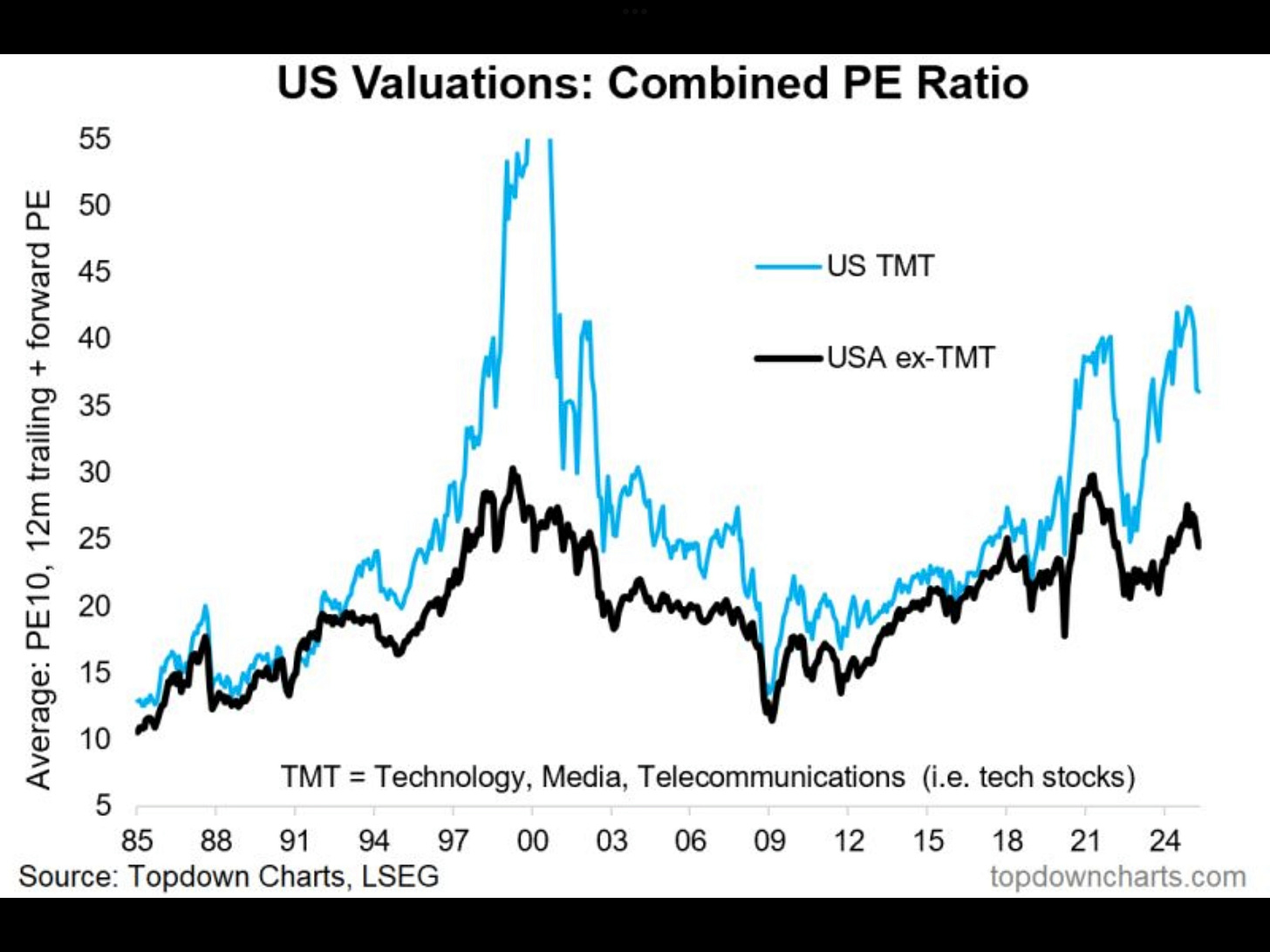

The Currency Debasement Factor: The Rising Tide Lifts Growth Boats: This is a theme regular readers will be very familiar with. I specifically wrote about it here. In an environment of persistent currency debasement – where, as I’ve argued, the real purchasing power of cash might be eroding by something like 8-10% annually due to monetary expansion and inflation – capital naturally seeks refuge and growth in assets that can outpace this erosion. Money flows towards companies that can grow their earnings at a significant nominal rate. This disproportionately benefits growth stocks and pushes their valuations higher. Investors are willing to pay a premium for companies that offer a credible path to outrunning the "melting ice cube" of fiat currency. This phenomenon really kicked off in earnest after the GFC in 2008, and the trend of higher valuations for growth assets (and thus for a growth-dominated index) has been pretty clear ever since. The market is simply reflecting the reality of the monetary environment. Look at the steady increase in the below chart after 2008.

So, these three factors – legitimate growth concentration, the changing composition of the index, and the powerful undercurrent of currency debasement – go a long way to justifying why the S&P 500's P/E ratio might be structurally higher today than in past decades, without necessarily signaling imminent doom.

But that's just justifying the present. What about the future?

Part 2: Why Today's Valuations Might Actually Be Cheap

Now, alongside these structural justifications for higher baseline valuations, there's another massive theme unfolding that I believe many are still underestimating: we are on the verge of an explosive technology boom powered by Artificial Intelligence.

The AI Investment Tsunami is Just Beginning: The amount of capital pouring into AI infrastructure and development is staggering. Nvidia's Jensen Huang recently projected that the annual investment in “AI Factories” alone could reach $1 trillion per year by 2030. This isn't just speculative venture capital; it's major corporations retooling their entire infrastructure for an AI-centric future.

Breakthroughs Accelerating: The speed of advancements in AI model capability (think language models, image generation, drug discovery, coding assistants, robotics) is unlike anything we've seen before. This, coupled with the massive increase in computing power coming online (thanks to companies like Nvidia), is set to turbocharge development across countless industries.

Killer Applications on the Horizon: We can already sense the paradigm shifts coming. Self-driving cars have moved from science fiction to reality. Humanoid robotics are making rapid progress, promising to revolutionize manufacturing, logistics, and everything else. These aren't just incremental improvements; they are entirely new markets worth trillions of dollars.

Big Tech: The Primary Beneficiaries (and Still Reasonably Valued?) Who stands to gain the most from this AI revolution? Unsurprisingly, it's the Big Tech incumbents who have the data, the talent, the existing platforms, and the capital to lead the charge. And here's the kicker: if you look at the current forward P/E ratios of companies like Google (around 17), Meta (around 26), or even Nvidia (around 30), given the almost unimaginable scale of the growth that AI could unlock for them, they might not look expensive at all. If they can capture even a fraction of these new AI-driven markets while also enhancing their existing businesses with AI, their future earnings growth could be truly explosive, making today's valuations seem quite reasonable, if not downright cheap, in a few years. Sadly, whether you think AI will take jobs or not won’t matter for the Magnificent 7. They will benefit regardless of how others battle with AI.

Conclusion: Seeing Through the Surface-Level Noise

So, when you hear the constant drumbeat about "historically overvalued markets," I encourage you to look below the surface. There are legitimate structural reasons why valuations appear higher today. The concentration of highly profitable growth in dominant tech companies, their increasing weight in the index, and the persistent tailwind of currency debasement all contribute to a new valuation paradigm.

And more importantly, if you believe, as I do, that we are at the foothills of a transformative AI-driven technology boom, then today's "high" valuations might not only be justified but could actually represent a compelling opportunity. The growth ahead could be far more significant than current multiples imply. As always, it's about thinking through the first-order effects and the critical second-order consequences.

However, if you’ll sleep better thinking it dot-com 2.0 then maybe just keep thinking that.